Analysis and prediction of a stock

Constructing model, predicting and using machine learning to predict a stock evolution

Context

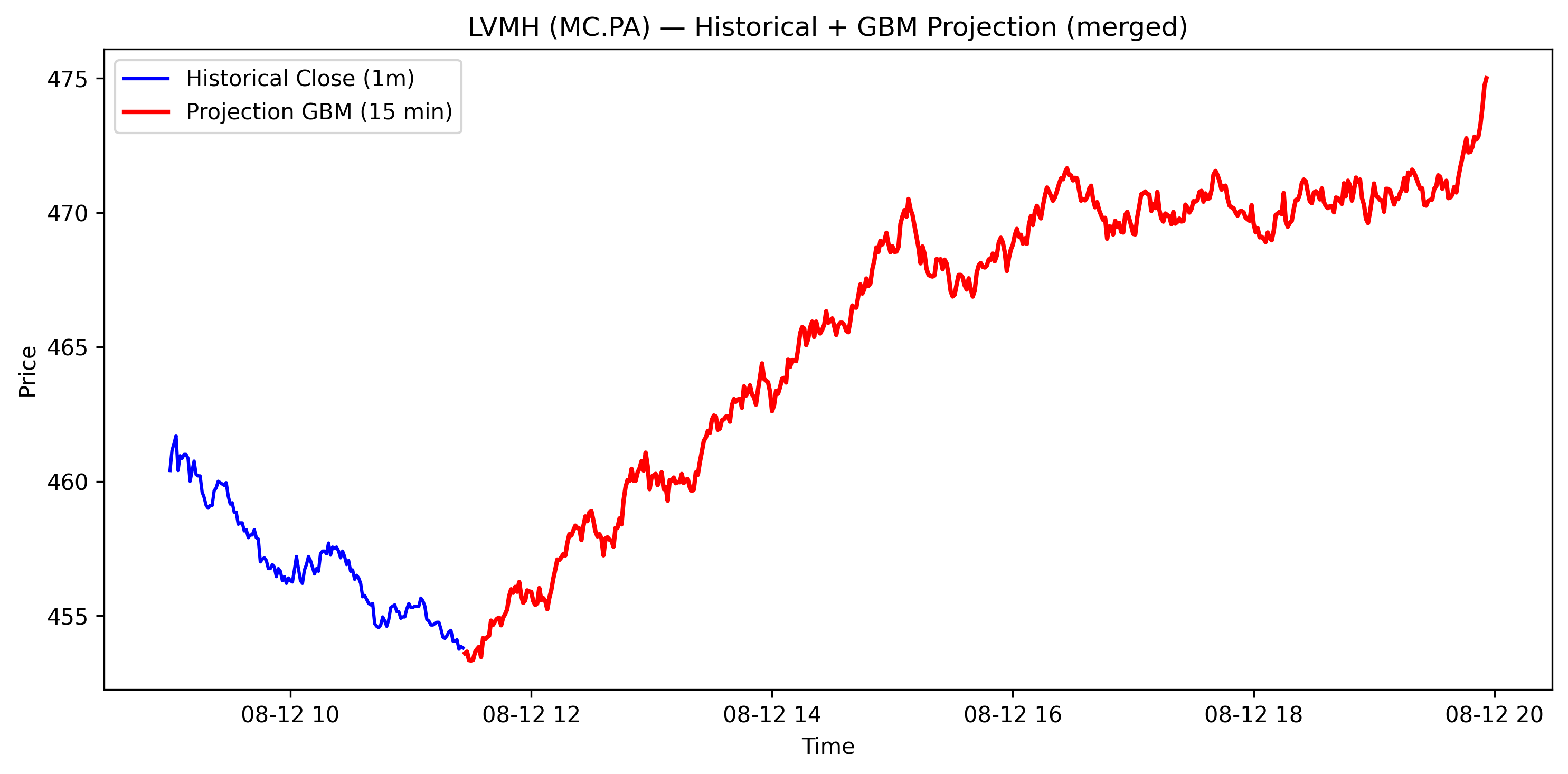

This project was a personal research initiative aimed at applying machine learning to real-time European stock market data—specifically, LVMH's (Moët Hennessy Louis Vuitton SE) trading on Euronext Paris. Constructing predictive models for stock evolution is vital for understanding market dynamics and making data-driven investment decisions. LVMH, as one of the flagship stocks in the CAC 40 index, provides a representative case study for building financial modeling skills.

Approach

- Data: Collected real-time price data from Euronext Paris for LVMH, cleaned and structured time series features (e.g., daily prices, volume, moving averages).

- Methods: Built predictive models using regression and ensemble algorithms (e.g., Random Forest), tuned hyperparameters, and evaluated performance using validation sets to select the best-fitting model.

- Management: Organized the project into phases: data acquisition, preprocessing, exploratory analysis, model development, evaluation, and deployment. Set milestones for each phase to ensure steady progress.

Results

This project sharpened my skills in efficient machine learning and hands-on use of financial APIs. I mastered the use of the Python yfinance library to reliably fetch historical stock data for modeling. Beyond code, I gained deeper proficiency in data analysis, model evaluation, and workflow automation—essential skills for turning raw data into actionable insights.